The Ozempic, Mounjaro, and GLP-1 Chapter in Your Restaurant's History

Let's start from the beginning.

What is GLP-1?

GLP-1 (Glucagon-Like Peptide-1) is a natural hormone produced in the intestine after meals, essential for regulating blood sugar, stimulating insulin, and increasing satiety.

GLP-1 agonist medications mimic this natural action and last much longer in the body. The mechanism is simple: they imitate the GLP-1 hormone, which signals fullness to the brain, slows gastric emptying, and dramatically reduces appetite. The practical result for those who use them is that small amounts of food already generate satisfaction.

Ozempic, Mounjaro, and Wegovy are the best known. But the list is already long — and is expected to grow significantly soon as patents expire.

The impact on eating habits — and on consumer behavior at bars and restaurants — is inevitable.

Will people stop going out to eat? Breakfast, lunch, or dinner: which out-of-home meal will be most affected? Do I need to expand my mocktail and protein options?

Let's take it step by step.

A lot is changing. We researched extensively — with our clients inside and outside Brazil, as well as international reports and articles — and we bring here the insights that will help you understand the landscape.

What we know for certain is that this wave has already arrived. Some are already riding it. Others are still waiting.

Let's break down each point.

The size of the phenomenon: numbers no manager can ignore

The global data is significant. Worldwide spending on GLP-1 medications surpassed $54 billion in 2024, and the market could reach between $100 and $150 billion annually by 2031 — compared to just $2.4 billion in 2021. In the United States, between 12% and 15% of households already have at least one user of these medications, representing between 45 and 50 million people. In a country where 42% of adults are obese — 110 million people — the growth potential is structural.

The impact on food consumption is already measurable: food spending drops an average of 5.3% after starting treatment — and reaches 8.2% in higher-income households, exactly the profile that frequents restaurants most. 73% of patients in treatment report eating less, and 85% develop an aversion to fat, sugar, or alcohol.

In Brazil, growth is also accelerating. And we don't need a report to feel it — anyone who attended New Year's Eve or Carnival this year noticed: the "newly slim" drew attention. You noticed too, right?

Estimates point to hundreds of thousands of patients on continuous monthly use — concentrated, for the most part, in the middle and upper income brackets of major cities. Exactly the customer profile that frequents restaurants.

The truth is: Your audience is already taking the medication

This is the central point that many entrepreneurs haven't yet internalized: the GLP-1 user is not some other audience. It is your audience. These are middle-to-upper income consumers, with intense urban routines, access to preventive healthcare, and a willingness to spend on quality gastronomic experiences.

These are exactly the people who frequent chef-driven restaurants, artisanal pizzerias, contemporary kitchen bars, and fine dining establishments.

What changes is not the desire to go out and eat. What changes is the consumption capacity per meal. Studies indicate that GLP-1 users decrease the number of items ordered per visit by just 1% — but they shift from sides to main dishes and increase demand for vegetables, fruits, and items with high nutritional value.

How the market is responding: lessons from the US, Europe, and Brazil

The market is already responding — and it reveals interesting patterns across three distinct geographies.

#1 — First insight: make your dish appetizing and healthy. Abundance and cost-effectiveness are no longer the main argument. Reflection: the customer is more selective, but still willing to pay well for an experience that justifies the outing. Those who understand this first will be ahead.

United States: Major Chains Rewrite Their Menus

The American market was the first to react at scale, and the cases of major chains are a reference map for any entrepreneur who wants to anticipate what will arrive in Brazil.

Chipotle launched the "High Protein Cup", with items ranging from 15 to 81 grams of protein. The chain bet on a high-protein, low-carb menu, creating a specific line for the eating behavior of GLP-1 users without needing to mention the medications explicitly.

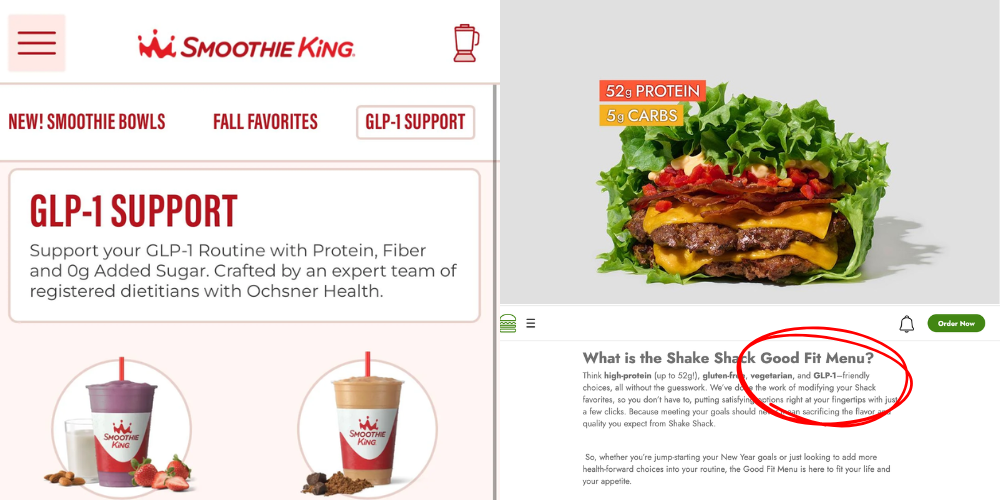

Shake Shack launched the "Good Fit Menu", with bun-free burgers delivering up to 52 grams of protein per serving. The messaging emphasizes performance and well-being — not dieting, not deprivation.

Olive Garden introduced a "lighter portions" menu, with reduced servings at lower prices. The chain made a direct bet on the volume-price equation, recognizing that part of its audience no longer wants — and can no longer eat — the house's traditional dishes.

Subway added "Protein Pockets" to the menu, a compact and protein-rich version of traditional sandwiches. Smaller format, clear nutritional proposition, without sacrificing the convenience that is the brand's DNA.

Smoothie King was even more direct: they launched a menu officially called "GLP-1 Support," with options developed to complement the treatment — focused on dense nutrition, protein, and functional ingredients. One of the few chains to explicitly name the medication in their communications.

The pattern that emerges from these initiatives is not simply "smaller portions." It's flexibility and protein. As the CEO of a New York hospitality group put it: "We're not shrinking the plates. We're changing how customers want to eat." The demand is not for less — it's for different.

Not everyone is on board, though. Celebrity chef Gordon Ramsay publicly declared he will not offer GLP-1 menus at his restaurants, calling the idea absurd. His position represents a bet on the customer who values the full experience, without concessions. It's a legitimate choice — but one that requires being clear about who your audience is and what your establishment stands for.

#2 — Second insight: It's not mandatory to follow the crowd, nor is it advisable. Understand your audience, observe and talk to them. See if it makes sense or not.

Europe: Luxury in Smaller Doses

In Europe, the trend arrives with an additional layer of sophistication. Fine dining restaurants in London and other European capitals have launched specific menus that promise "the full luxury experience in smaller volume." The proposition is not one of deprivation — it's curation. Smaller dishes, with premium ingredients, presented carefully and priced proportionally. Michelin-starred establishments are already formally offering reduced tasting options explicitly framed around wellness and mindful eating.

#3 — Third insight: reducing volume does not have to mean reducing the ticket. On the contrary, it can raise it — as long as the value proposition is built correctly.

São Paulo: Discreet but Strategic Adaptation

In Brazil's capital, restaurants of different profiles have begun noticing changes in table behavior: larger groups sharing the same dish, lower alcohol consumption, and growing demand for smaller versions of traditional dishes. Establishments that historically sold generous portions have begun offering smaller options — not as replacements, but as strategic menu alternatives. Operators prefer to frame them within concepts such as "tasting experience," "omakase," or "sharing portions."

CONCLUSION: GLP-1 is just one more chapter. Your restaurant is the story.

You, chefs and entrepreneurs, know better than anyone: trends come and go. But restaurants go beyond. They always have.

Sitting at a table in a café, restaurant, or bar is socialization, experience, relaxation, meetings, encounters, conversation — and sometimes even reflection. That fits in no prescription insert — and no medication changes that.

What is fundamental, however, is understanding what is happening around you and having the ability to adapt without losing your essence. What sustains a real business is not the trend you followed — it's the reputation you built, the communication you kept consistent, and the differentiator that became clear to your customer over time.

A well-written piece! The core message is that GLP-1 medications are reshaping how restaurant patrons eat — not whether they go out — and that smart operators should adapt their menus toward protein-rich, nutrient-dense, and smaller-but-premium options rather than simply shrinking portions or chasing the trend blindly.